Callable Bonds: Be Aware That Your Issuer May Come Calling

Therefore, they often include a call feature in their issues that provides them a means of refunding a long-term issue early if rates decline sharply. Although the prospects of a higher coupon rate may make callable bonds more attractive, call provisions can come as a shock. Even though the issuer might pay you a bonus when the bond is called, you could still end up losing money. Plus, you might not be able to reinvest the cash at a similar rate of return, which can disrupt your portfolio.

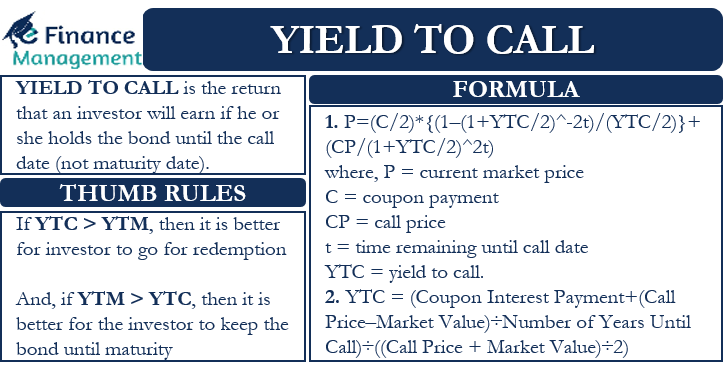

Analyzing Callable Bonds

When analyzing callable bonds, one bond isn’t necessarily more or less likely to be called than another of similar quality. The main factor that callable bond meaning causes an issuer to call its bonds is interest rates. One feature, however, that you want to look for in a callable bond is call protection.

Understanding Callable Securities

An investor purchases $10,000 worth and receives coupon payments of 6% x $10,000 or $600 annually. Three years after issuance, the interest rates fall to 4%, and the issuer calls the bond. The bondholder must turn in the bond to get back the principal, and no further interest is paid. Fixed-income investors in low-interest-rate environments often discover that the higher rate they receive from their current bonds and CDs doesn’t last until maturity. In many cases, they will receive a notice from their issuers stating that their principal is going to be refunded at a specific date in the future.

Do investors like callable bonds?

You can invest in stocks, exchange-traded funds (ETFs), mutual funds, alternative funds, and more. SoFi doesn’t charge commissions, but other fees apply (full fee disclosure here). SoFi has no control over the content, products or services offered nor the security or privacy of information transmitted to others via their website.

When that happens, they can pay back the principal of existing bonds, then issue new ones at lower interest rates. Just as you might want to refinance your 6% mortgage if interest rates dropped to 3%, Company XYZ will want to refinance its debt to save money on interest. Issuers typically include a call provision that allows them to redeem their bonds early, which allows them to refinance the debt at a lower interest rate. It’s important to keep in mind the pros and cons of investing in callable bonds when considering a long-term investing strategy.

- A callable security is a bond or other type of security issued with an embedded call provision that allows the issuer to repurchase or redeem the security by a specified date.

- Investors should carefully consider the call features, credit rating, and time to maturity when evaluating callable bonds for investment.

- If you are looking to invest in a callable bond, you should do this after carefully analysing the bond document that explains all the terms and conditions of recall.

- A bank might stipulate that the company reduce its debt before it can get approved for the loan or an extension of an existing credit line.

Since investors might have their callable bond redeemed before maturity, investors are compensated with a higher interest rate when compared to the traditional, noncallable bonds. Sinking fund redemption requires the issuer to adhere to a set schedule while redeeming a portion or all of its bonds. A sinking fund helps the company save money over time to avoid a large lump-sum payment to pay off the bond at maturity. A sinking fund has bonds issued whereby some of them are callable in order for the company to pay off its debt early. Three years after issuance, the interest rates fall to 4%, and the bond is called by the issuer.

Finally, you can employ certain bond strategies to help protect your portfolio from call risk. Laddering, for example, is the practice of buying bonds with different maturity dates. If you have a laddered portfolio and some of your bonds are called, your other bonds with many years left until maturity may still be new enough to be under call protection. And your bonds nearer maturity won’t be called, because the costs of calling the issue wouldn’t be worth it for the company. While only some bonds are at risk of being called, your overall portfolio remains stable.

Therefore, issuers must pay higher interest rates to persuade people to invest in them. Usually, when an investor wants a bond at a higher interest rate, they must pay a bond premium, meaning that they pay more than the face value for the bond. With a callable bond, however, the investor can receive higher interest payments without a bond premium. Many of them end up paying interest for the full term, and the investor reaps the benefits of higher interest the entire time.

Investors can use callable bonds to hedge against interest rate risk by buying bonds with different call features and maturities. This strategy can help protect the portfolio’s value in various interest rate environments. Multi-callable bonds can be called on multiple specified dates, giving issuers even more flexibility in managing their debt obligations. American callable bonds allow issuers to call the bonds at any time after the call protection period has expired.

The company might want to increase the loan amount, or if no loan exists, get approved for a new loan. A bank might stipulate that the company reduce its debt before it can get approved for the loan or an extension of an existing credit line. Before a bank lends to a corporation, they will analyze the company’s financial statements, revenue outlook, profitability, and the amount of debt a company is carrying on its balance sheet.